Imagine you are living a good life in a big metro city, but something happens and you suddenly get into a medical emergency. Now what? The truth is that life is unpredictable, and health insurance is essential to protect against any unpredictable medical emergency expenses.

Health insurance covers expenses related to illness, injury, and preventive care. But, here is the catch! Selecting the right health insurance in Delhi–like cities is important because, without it, you may fall into scam traps and over-complicated conditions and lose all your money. Moreover, choosing the right policy can save you money, offer more returns in coverage, cut costs, and offer a network.

An informed decision helps individuals select a plan that fits their healthcare needs and budget. Moreover, they avoid unexpected expenses and ensure protection for your family & yourself.

But more of anything, the right health insurance offers better health outcomes and peace of mind which is essential in today’s complex & fast lifestyle. So how can you find the right health insurance companies in Delhi?

Read our blog completely and get everything you should know!

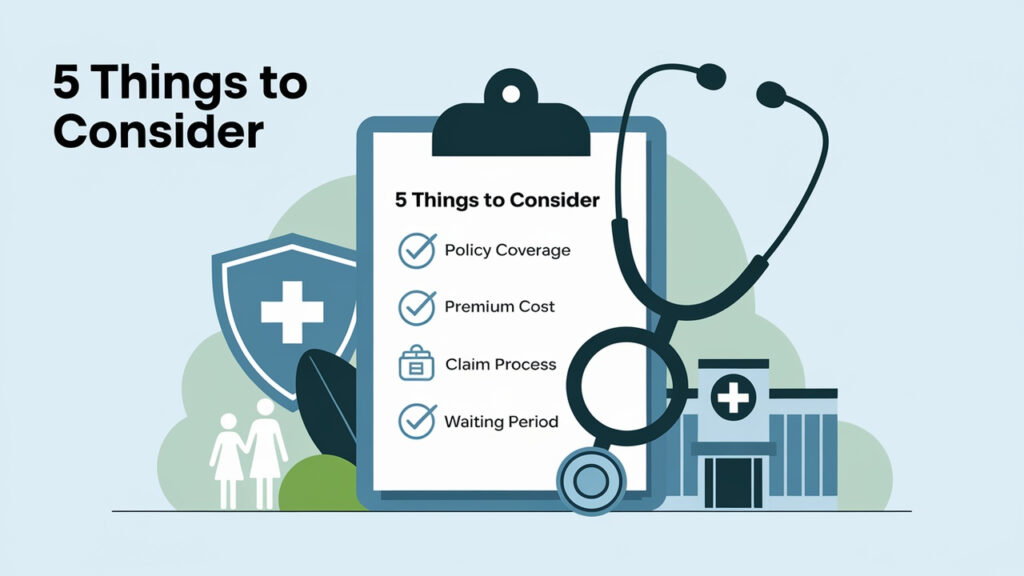

Here are 5 Things You Must Consider Before Buying Health Insurance:

1. Coverage & Sum Insured

The SUM INSURED is the maximum amount an insurance company will pay for medical expenses in a year. Choosing the right sum insured is important because it will help avoid any kind of medical financial crisis.

With the wrong coverage and sum insured, you will have extra money from your pockets for medical and doctor’s fees. This will surely cause a headache to your financial conditions. A higher sum insured and coverage provide you a financial cushion, helps you to save more, and reduce stress.

Points to Consider Based on Age, Family Size, and Health History:

- Age: Older individuals may need higher coverage. This is due to their higher potential health risks.

- Family Size: Family health insurance should cover your whole family. So, before you sign up, make sure the sum is shared among all the family members. Note- large families will need higher coverage too, so check the offered plan thoroughly.

- Health History: Any pre-existing health conditions can increase coverage to manage the ongoing treatment costs. People having heart issues must look for a higher sum insured.

2. Network Hospitals

It is important to ensure the hospitals are in the network. Make sure that the network hospitals offer cashless facilities in their centre. This reduces the hassle during emergencies. Choosing an insurance company that offers the right network of hospitals near your location.

But why check these benefits in the first place?

Cashless facilities make the payment procedure faster and easier. This allows patients to receive treatment without paying upfront at hospitals.

This whole scenario minimises the financial and administrative burden on family members. And not to mention, this is especially beneficial for senior citizens or people with special medical needs.

3. Inclusions and Exclusions

Before you sign up for an insurance policy, make sure to understand thoroughly what the policy covers vs what it doesn’t. Health insurance typically covers the following.

- Hospitalization

- Surgeries

- Day-care procedures

- Pre and post-hospitalization expenses

- Ambulance charges

- Outpatient treatments (Sometimes).

However, here are some of the most common exclusions:

- Cosmetic surgeries

- Certain pre-existing conditions during the waiting period.

- Non-medical expenses.

Importance of Reading the Fine Print

You need to be careful while reading the policies of an insurance company. Because it deals with your coverage and actual payment, pay attention to some of the following offerings.

- Waiting period.

- Co-payment clauses

- Coverage limits.

- Exclusions.

- Renewal terms.

Reading all these will prevent any unfortunate claim issues and help you in emergencies.

4. Waiting Period & Pre-existing Conditions

The next thing you must consider is to check the waiting period and pre-existing health conditions. Here is a short intro to the term.

Waiting Period– Most health insurance plans impose a waiting period before you can claim their health insurance coverage for specific pre-existing conditions. Most insurance offers 1-4 years of waiting period only. This means you will not be paid during the waiting period.

So, if you have any kind of pre-existing health issues, make sure to choose a policy that has shorter gaps in protection or provides immediate coverage only from the very start.

Choosing the right one will support you financially for ongoing treatments or may reduce the gaps in protection.

5. Claim Settlement Ratio & Insurance Provider Reputation:

Here is a brief definition of the term.

1. Claim Settlement Ratio:

This term indicates the percentage of claims an insurance company settles against the total claims. A higher CSR means the company is more reliable and keeps its customers in check in difficult times.

This ratio helps you to understand how much insurance companies in Delhi care about your health and whether it will be a good choice for your trust. When buying an insurance policy, this should be your top factor to check.

2. Why is this important?

Good customer service, transparent claim processes, and the reputation of an insurance company help you to get a hassle-free experience.

Choosing a reputed insurance company reduces the risks of claim rejection and delays.

This helps you to select a health insurance plan with good monetary help in the worst situations.

Conclusion:

Are you looking for a reliable and trusted insurance policy in Delhi to prevent any unfortunate events in the future?

Bravo! You are thinking in the right direction. You should buy insurance, but you need to check these 5 factors before you invest your money into one i.e. coverage and sum insured, network hospitals and cashless facilities, inclusion and exclusions of the coverage, waiting period, and pre-existing health condition coverage policies, claim settlements ratio.

However, here is an additional PRO TIP for you- Before you buy any insurance policy, consider consulting with an expert.